The Broken Correlation

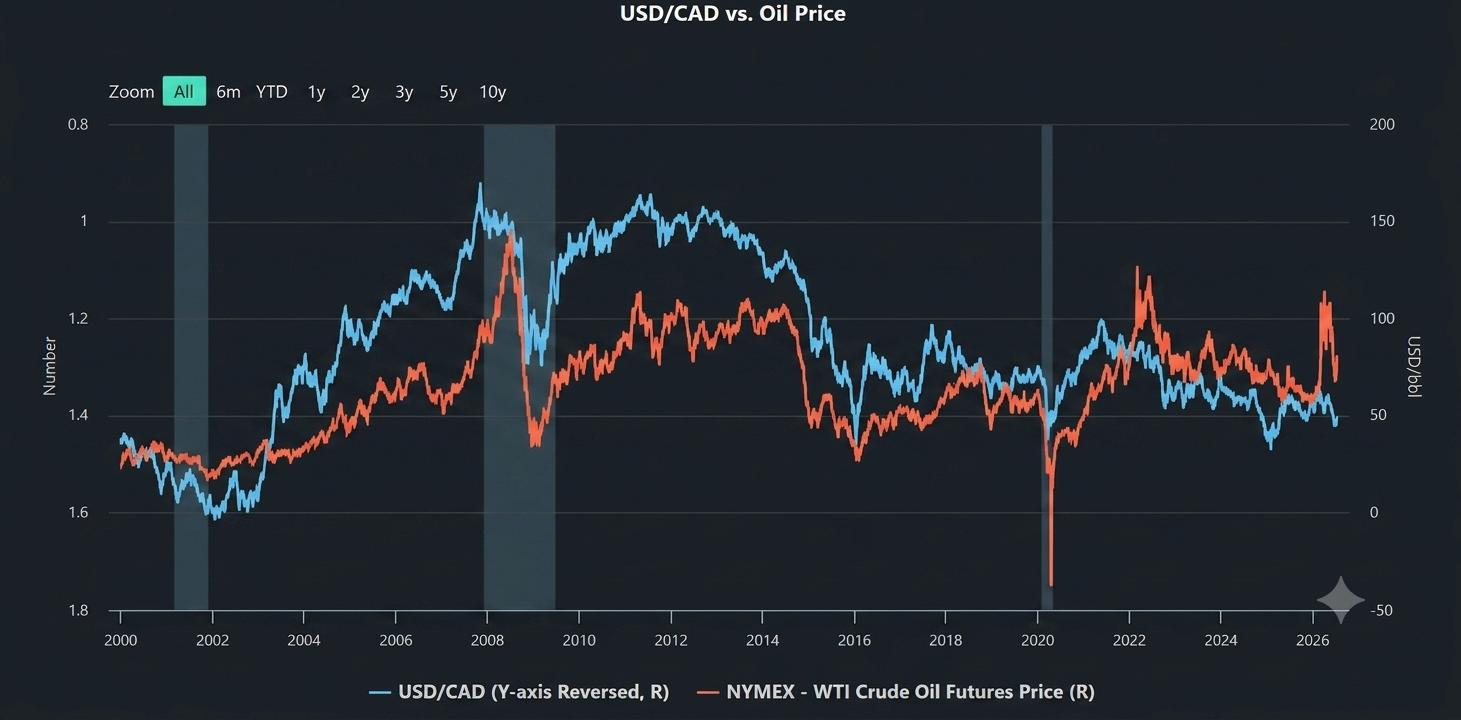

For over two decades, one of the most reliable mechanical relationships in the foreign exchange market was the positive correlation between crude oil prices and the Canadian Dollar. As a G10 economy and one of the world’s largest net exporters of energy, Canada’s terms of trade have historically been tethered directly to the energy complex. Under standard market conditions, when crude oil prices rally, Canada’s export revenues surge, trade balances improve dramatically, and the Bank of Canada (BoC) adopts a more hawkish tone to curb domestic demand. This fundamental loop inevitably drove the USD/CAD currency pair lower.

Yet, as global financial markets navigate the high-volatility regime of mid-May 2026, this reliable textbook correlation has broken down. With Brent crude oil surging past $105 per barrel due to intensifying geopolitical stress in West Asia and maritime threats around the strategic bottleneck of the Strait of Hormuz, the Canadian Dollar has failed to stage a reciprocal rally. Instead of plunging toward historical multi-year lows, USD/CAD remains stubbornly elevated, fluctuating wildly and trapping retail breakout traders.

This is the ultimate market tug-of-war. To trade this environment successfully, market participants must look beyond simple price patterns and understand the structural forces preventing the Loonie from capitalizing on its energy advantage.

The Safe-Haven Paradox: When Risk Off Trumps Commodities

The primary force paralyzing the Canadian Dollar is the global flight to quality. While Canada benefits on a purely commercial front from high energy prices, the cause of the current oil spike is fundamentally geopolitical and inflationary. When energy markets experience an aggressive supply-side shock due to maritime choke point disruptions, it acts as a massive tax on global economic growth.

In this scenario, international fund managers do not chase commodity currencies; they seek immediate shelter in the world’s absolute reserve currency, the U.S. Dollar.

This creates the Safe-Haven Paradox. The commercial benefit of $105/bbl oil entering Canadian ports is entirely neutralized by the sheer volume of global capital fleeing European, Asian, and emerging markets to buy highly liquid, Dollar-denominated safe-haven assets. Because oil is priced globally in USD, an energy crisis paradoxically increases the transactional demand for the Greenback.

When global markets enter periods of high volatility, asset managers liquidate foreign positions and convert funds back into U.S. Dollars. The Canadian Dollar, despite its energy cushion, is still classified globally as a risk-sensitive, cyclical asset. When global risk sentiment turns exceptionally thin, the broad “risk-off” liquidation flow routinely overpowers localized export revenue dynamics, keeping USD/CAD locked in a defensive stance.

To trace how this baseline behavior has completely shifted the currency landscape this year, review the analysis on decoupled historical correlations.

Real Yield Differentials and the Monetary Policy Divergence

Beyond sentiment, the structural floor beneath USD/CAD is being reinforced by fixed-income markets, specifically the shifting spread between U.S. Treasuries and Canadian Government Bonds (GoCs). Persistent energy inflation has severely complicated the forward guidance of major central banks. As transportation and global manufacturing costs scale upward, the Federal Reserve is forced into a restrictive posture, maintaining high interest rates for longer than the market previously discounted.

According to the CME FedWatch Tool, traders have aggressively scaled back expectations for Federal Reserve monetary easing as energy-driven risks accelerate inflation expectations. This has caused the U.S. Treasury yields to climb rapidly. To observe how this massive shift towards the greenback is developing in real-time, institutional traders monitor the ongoing aggressive safe-haven demand for the U.S. Dollar.

Meanwhile, the Bank of Canada faces a much more delicate balancing act. Although the BoC recently delivered a hawkish hold, acknowledging that oil boosts nominal export revenues, the central bank is highly aware that sustained $100+ oil acts as a severe, regressive tax on the domestic Canadian consumer. Canada’s economy features highly sensitive debt profiles, leaving it more vulnerable to prolonged restrictive interest rates than the United States.

Because the Federal Reserve has a more aggressive runway to maintain tight financial conditions, the real yield spread (the inflation-adjusted interest rate differential) favors the United States. Institutional capital flows naturally toward the higher-yielding asset when adjusted for risk. Therefore, even though Canada’s trade balance is in a surplus, the macroeconomic capital account flows strongly out of the CAD and into the USD to capture these superior U.S. yields, forming a persistent bullish trendline that resists downward pressure.

Retail Sentiment Illusion and Institutional Liquidity

A major operational hazard in the current environment is the proliferation of “narrative trading” among retail communities on platforms like Reddit and TradingView. Retail traders often look at a chart of surging WTI or Brent crude and blindly market-buy the CAD or short the USD/CAD, assuming the historical correlation must eventually snap back into place. This creates highly concentrated, emotional positioning near major technical levels.

Institutional market makers and algorithmic systems track this retail positioning carefully. When retail sentiment becomes heavily lopsided, it creates immense pools of liquidity (stop-losses and buy-stops) just above major multi-month resistance levels and trendlines.

Institutional participants may seek to exploit these crowded trades. Instead of blindly following the retail social momentum, institutional desks utilize retail positioning as a contrarian indicator. They wait for an oil headline to spike the market, watch retail traders aggressively chase the move, and then step in to sweep the liquidity, triggering sharp bull traps and violent whipsaws. Professional traders understand that by the time an “energy trade” becomes overwhelmingly popular online, the underlying move has already been entirely priced in by institutional capital.

Final Thoughts: Navigating the New Macro Regime

The structural breakdown of the historical oil-Lonie correlation serves as a powerful reminder that currency markets in 2026 do not operate on static, linear rules. While the commercial benefits of $105+ Brent crude continue to support Canada’s underlying trade balance, this factor is currently being entirely dominated by the broader capital account dynamics. The combination of intense safe-haven flows into the U.S. Dollar and a widening real yield differential (driven by a highly restrictive Federal Reserve) creates an invisible, resilient floor that prevents USD/CAD from collapsing. To monitor the direct interaction between global balance of payments and these institutional safe-haven allocations, professional desks track the Trading Economics Capital Account Data to isolate net flows.

For institutional and professional traders, success in this environment requires abandoning old retail biases. Trying to short USD/CAD simply because “oil is making new highs” is a dangerous strategy that ignores market micro-structure and cross-asset capital flows. The current market regime rewards tactical flexibility, deep fixed-income integration, and strict risk discipline. By shifting your focus from isolated price action to the fundamental forces driving global liquidity, you can avoid the emotional traps of narrative trading and secure a genuine, sustainable edge in the foreign exchange complex.

FAQ: USD/CAD & Energy Market Dynamics

1. If Canada is running a massive trade surplus due to high oil prices, why isn’t the CAD outperforming the USD?

In the current macro environment, the Capital Account is completely overpowering the Trade Account. While it is true that more nominal revenue is flowing into Canadian ports from energy exports, the global geopolitical crisis is simultaneously triggering an aggressive flight to quality.

Because the U.S. Dollar is the absolute global reserve currency, international asset managers are liquidating global exposures and converting funds into USD-denominated assets. This safe-haven demand, combined with superior U.S. Treasury yields, creates a structural capital inflow into the Greenback that easily neutralizes the localized commercial strength of the Canadian Dollar.

2. How exactly does the U.S. 10-Year Treasury yield protect the USD/CAD from dropping during an oil rally?

High oil prices act as a regressive tax on global growth while stoking persistent inflationary pressures. This forces the Federal Reserve to maintain an aggressively restrictive monetary policy stance, the well-known “Higher for Longer” approach. As a result, U.S. Treasury yields climb rapidly.

If the spread between the U.S. 10-Year Treasury and the Canadian Government Bond (GoC) widens in favor of the United States, institutional capital will naturally flow out of the CAD and into the USD to capture these higher, risk-adjusted yields. This real yield differential acts as a powerful fundamental cushion, keeping USD/CAD elevated despite surging crude prices.

3. How do institutional algorithms exploit retail “narrative trading” near major technical levels on USD/CAD?

Retail trading communities frequently rely on lagging indicators or oversimplified historical correlations, assuming that USD/CAD must drop when crude oil rallies. This leads to highly concentrated, one-sided retail short positioning near major resistance zones and trendlines.

Institutional market makers and algorithmic execution desks monitor this lopsided sentiment as a contrarian indicator. They wait for a fresh energy headline to spike the market, watch retail traders aggressively chase the move, and then trigger sharp liquidity sweeps, resulting in violent bull traps and whipsaws that stop out retail accounts while accumulating institutional positions at highly favorable prices.

4. What specific macroeconomic developments could cause the USD/CAD correlation to normalise and send the pair sharply lower?

For the historical negative correlation to reassert itself and drive USD/CAD aggressively lower, the market requires a structural shift in global risk distribution. First, a verifiable de-escalation of geopolitical tensions around maritime choke points would strip the safe-haven premium out of the Greenback. Second, a stabilization of Canadian domestic credit conditions would allow the Bank of Canada to match or exceed the Federal Reserve’s restrictive posture, thereby compressing the real yield differential. Finally, high oil prices would need to be driven by organic expansion in global manufacturing and consumer demand rather than artificial supply-side constraints, allowing commodity-linked capital inflows to dominate daily price action.

5. Is it safe to execute trend-following strategies on USD/CAD when crude oil spikes during the Asian market session?

Executing trend-following breakout strategies during the Asian session carries an exceptionally high risk of capital impairment. The Asian session features substantially lower liquidity for the Canadian Dollar complex compared to the London and New York crossover. When an unexpected energy headline drops during these hours, market makers aggressively widen out their bid-ask spreads to mitigate risk, which results in severe slippage on market orders. Because institutional desks may use these thin-liquidity windows to trigger stop-loss hunts, these sudden moves can turn into bull or bear traps, making it prudent for professional traders to utilize strict limit orders and wait for Europe to open before deploying fresh capital.

Disclaimer: The content of this article is intended for informational purposes only and should not be considered professional advice.