Updated: April 2026 by Aaron Akwu.

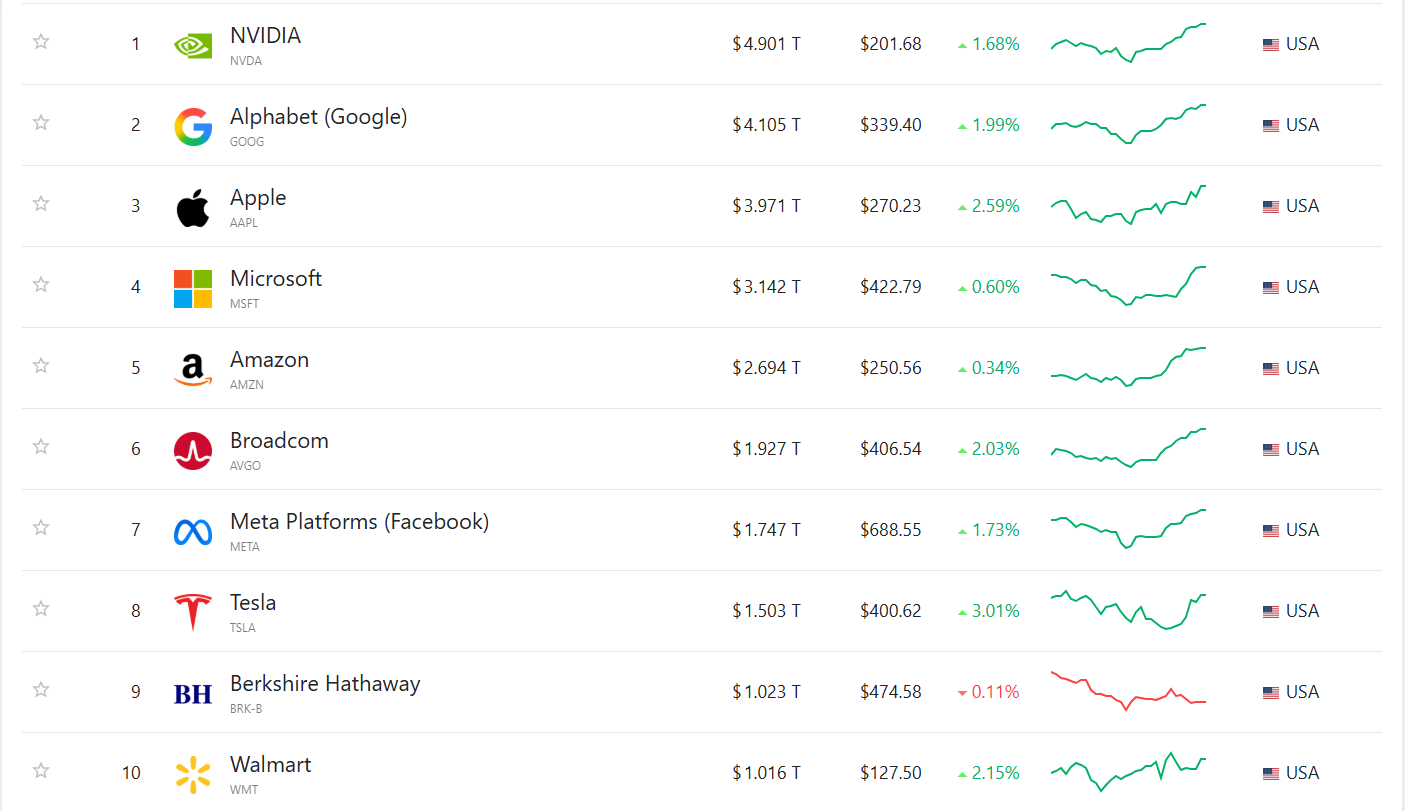

The latest ranking of the largest US companies by market capitalisation shows that AI and cloud-related momentum continue to reshape the top of the market. NVIDIA remains firmly in first place, while Apple has moved up by one position and Alphabet has climbed by two. Microsoft and Amazon have slipped slightly in the ranking, not because of fundamental weakness, but because rivals have advanced faster. Meanwhile, Walmart has entered the top 10, replacing JPMorgan Chase and highlighting the growing strength of large-scale retail alongside the continued dominance of technology firms.

Why Market Capitalisation Matters for Traders

Market capitalisation is the total market value of a company’s outstanding shares. For traders, it is more than just a size metric. It reflects investor confidence, affects index weighting in benchmarks such as the S&P 500 and Nasdaq-100, and often correlates with liquidity, volatility, and institutional attention.

These mega-cap companies are not just corporate giants. They are market leaders that can influence entire sectors. Earnings, guidance, or strategic announcements from companies like NVIDIA, Apple, or Microsoft can move broader indices and shape sentiment across global markets.

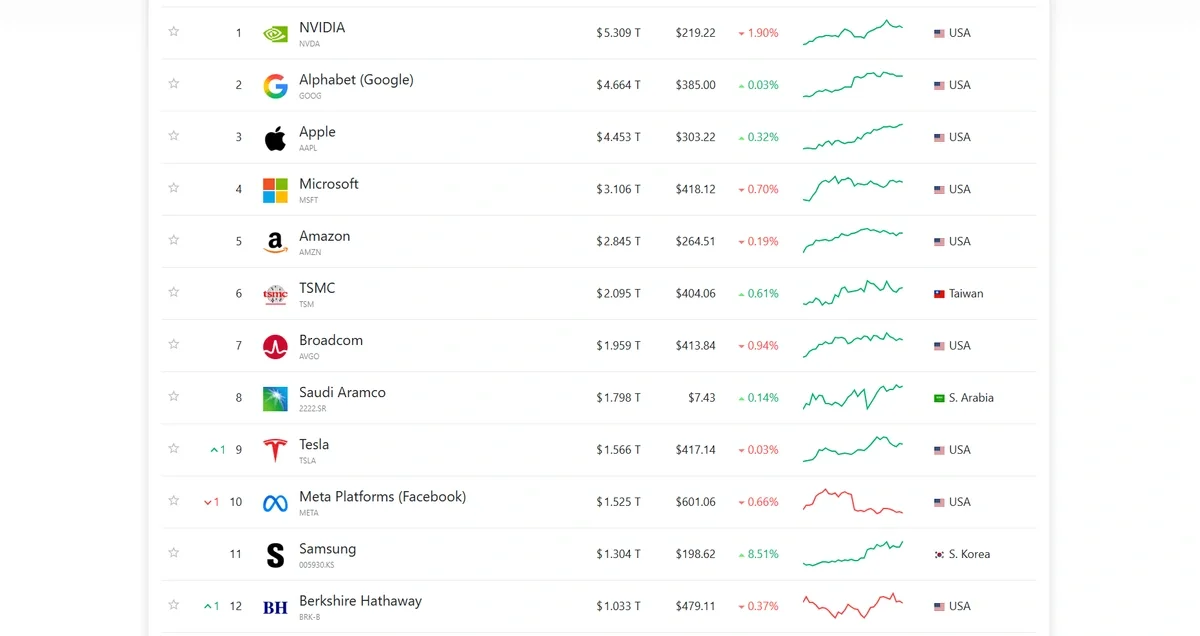

10 Largest US Companies

| Rank | Company | Ticker | Market Cap |

|---|---|---|---|

| 1 | NVIDIA | NVDA | $4.901 trillions |

| 2 | Alphabet (Google) | GOOG | $4.105 trillions |

| 3 | Apple | AAPL | $3.971 trillions |

| 4 | Microsoft | MSFT | $3.142 trillions |

| 5 | Amazon | AMZN | $2.694 trillions |

| 6 | Broadcom | AVGO | $1.927 trillions |

| 7 | Meta Platforms | META | $1.747 trillions |

| 8 | Tesla | TSLA | $1.503 trillions |

| 9 | Berkshire Hathaway | BRKB | $1.023 trillions |

| 10 | Wallmart | WMT | $1.016 trillions |

*According to CompaniesMarketCap.com

1. NVIDIA (NVDA)

![]()

NVIDIA designs and manufactures graphics processing units (GPUs) and AI computing platforms used in gaming, data centres, professional visualisation, and autonomous systems.

NVIDIA’s GPUs are the de facto standard for training and running large AI models. Its CUDA software ecosystem creates high switching costs, making it indispensable to the global AI infrastructure build-out.

Key business segments:

- Data Centre (AI chips, networking, enterprise AI platforms)

- Gaming (GeForce GPUs, gaming laptops, cloud gaming)

- Professional Visualization (RTX, Omniverse, creative and AI tools)

- Automotive (DRIVE platform for autonomous vehicles)

Growth drivers:

- Enterprise and sovereign AI adoption accelerating globally

- Blackwell architecture ramping through 2026

- Expansion into AI-powered robotics and edge computing

According to market consensus, NVIDIA’s data centre revenue is expected to grow around 35% to 40% year over year next quarter, with Blackwell shipments becoming a more meaningful contributor to results.

2. Alphabet (GOOG)

![]()

Alphabet is the parent company of Google, operating the world’s leading search engine, YouTube, Android, Google Cloud, and a portfolio of innovation-focused Other Bets.

Google Search and YouTube command unmatched scale in digital advertising, while Google Cloud has emerged as a credible number three player in global cloud infrastructure with strong AI differentiation.

Key business segments:

- Google Services (Search, YouTube, Android, Maps, Ads)

- Google Cloud (infrastructure, AI and machine learning tools, Workspace, security)

- Other Bets (Waymo, Verily, and frontier technology ventures)

Growth drivers:

- Gemini AI integration across Search, Workspace, and Cloud products

- YouTube Shorts and connected TV advertising growth

- Enterprise adoption of Google Cloud’s AI and data analytics tools

Consensus forecasts suggest Google Cloud revenue could grow at roughly 30% next quarter, with AI-related workloads accounting for an increasing share of new bookings.

3. Apple (AAPL)

![]()

Apple designs, manufactures, and sells consumer electronics, software, and services, including the iPhone, Mac, iPad, Apple Watch, and a rapidly growing subscription ecosystem.

Apple’s vertically integrated hardware-software ecosystem drives unmatched customer loyalty, pricing power, and high-margin recurring revenue through its Services business.

Key business segments:

- iPhone

- Services (App Store, iCloud, Apple Music, AppleCare, licensing)

- Wearables, Home and Accessories

- Mac and iPad

Growth drivers:

- Apple Intelligence features supporting future upgrade cycles

- Services segment continuing to expand at strong margins

- Emerging market penetration, especially in India and Southeast Asia

Analysts broadly expect low-to-mid single-digit revenue growth next quarter, with Services likely to remain the main margin driver and outperform hardware.

4. Microsoft (MSFT)

Microsoft develops enterprise and consumer software, cloud infrastructure, AI tools, and hardware, including Windows, Microsoft 365, Azure, Xbox, and LinkedIn.

Microsoft’s dominance in enterprise software, combined with Azure’s position as the number two cloud platform and its early lead in commercial AI through Copilot, gives it one of the most diversified and durable growth engines in the market.

Key business segments:

- Intelligent Cloud (Azure, server products, enterprise services)

- Productivity and Business Processes (Office 365, LinkedIn, Dynamics)

- More Personal Computing (Windows, Xbox, Surface, Search advertising)

Growth drivers:

- Azure AI services and Copilot adoption across enterprise customers

- Hybrid cloud and cybersecurity demand

- Gaming ecosystem expansion following Activision Blizzard integration

Azure revenue growth is expected to remain strong at around 25% to 30% year-over-year next quarter, with AI workloads contributing significantly to that expansion.

5. Amazon (AMZN)

![]()

Amazon operates the world’s largest e-commerce marketplace and is a global leader in cloud computing through AWS, digital advertising, logistics, and subscription services.

Amazon’s two profit engines, AWS and its scale-driven retail platform, create powerful network effects, data advantages, and customer lock-in across both consumer and enterprise markets.

Key business segments:

- Amazon Web Services

- North America and International e-commerce

- Advertising

- Subscription services (Prime, Twitch, Audible, MGM content)

Growth drivers:

- AWS re-acceleration supported by generative AI infrastructure demand

- Advertising business continuing to scale

- Fulfilment network automation improving efficiency and margins

Analyst estimates suggest AWS revenue growth could reach around 18% to 20% year over year next quarter, supported by rising enterprise demand for generative AI services.

6. Broadcom (AVGO)

![]()

Broadcom designs and supplies semiconductor and infrastructure software solutions for data centres, networking, broadband, wireless, and industrial applications.

Broadcom’s custom AI chips for hyperscalers, together with its mission-critical networking and infrastructure software portfolio, position it as a major beneficiary of enterprise and cloud AI spending.

Key business segments:

- Semiconductor Solutions

- Infrastructure Software

- Custom silicon programs for major cloud customers

Growth drivers:

- Rising demand for custom AI networking and accelerator chips

- VMware integration driving software synergies

- Growth in edge computing and enterprise connectivity

Street forecasts point to semiconductor revenue growth of roughly 25% year over year next quarter, led by continued AI-related demand from cloud providers.

7. Meta Platforms (META)

![]()

Meta operates Facebook, Instagram, WhatsApp, and Messenger, while also investing heavily in AI, virtual reality, and the metaverse.

Meta’s platforms reach billions of daily users, giving it unmatched scale in social media advertising. Its AI investments are improving ad targeting, engagement, and operational efficiency across the business.

Key business segments:

- Family of Apps

- Reality Labs

- AI infrastructure and recommendation systems

Growth drivers:

- AI-powered ad tools increasing advertiser return on investment

- Reels monetisation improving

- Continued cost discipline supporting margins

Consensus estimates indicate advertising revenue may grow in the low-to-mid teens next quarter, helped by stronger engagement and better AI-driven ad relevance.

8. Tesla (TSLA)

![]()

Tesla designs, manufactures, and sells electric vehicles, battery energy storage systems, solar products, and is also developing autonomous driving software.

Tesla remains a leader in EV brand strength, vertical integration, and real-world autonomous driving data, giving it a potential edge as the car industry becomes increasingly software-driven.

Key business segments:

- Automotive

- Energy Generation and Storage

- Services and Other

Growth drivers:

- Launch of a more affordable next-generation vehicle platform

- Full Self-Driving adoption and regulatory progress

- Expansion of energy storage deployments globally

Analysts expect vehicle delivery growth to remain relatively modest next quarter, with energy storage and services providing potential upside.

9. Berkshire Hathaway (BRK-B)

![]()

Berkshire Hathaway is a multinational holding company with wholly owned businesses and major equity stakes across insurance, transport, utilities, and consumer sectors.

Berkshire’s disciplined capital allocation, strong balance sheet, and broad portfolio of cash-generative businesses give it resilience, optionality, and defensive appeal during uncertain market periods.

Key business segments:

- Insurance

- Railroads and Utilities

- Equity Portfolio

- Manufacturing, Service and Retailing

Growth drivers:

- Strategic use of large cash reserves during market dislocations

- Ongoing buybacks when valuation is attractive

- Long-term earnings growth from operating subsidiaries

Consensus expectations suggest operating earnings could grow at a mid-single-digit pace next quarter, with insurance performance and rail volumes among the main swing factors.

10. Walmart (WMT)

![]()

Walmart is the world’s largest retailer by revenue, operating supercentres, neighbourhood markets, Sam’s Club locations, and an increasingly important e-commerce and advertising platform.

Walmart’s scale, supply chain efficiency, and omnichannel execution allow it to defend price leadership while expanding into higher-margin digital and advertising businesses.

Key business segments:

- Walmart US

- Walmart International

- Sam’s Club

- Advertising and Marketplace

Growth drivers:

- E-commerce and omnichannel fulfilment expansion

- Walmart Connect advertising growth

- Automation and AI-driven supply chain improvements

Analysts expect comparable sales growth of around 3% to 4% next quarter, with e-commerce likely to rise at a high-teens rate and advertising remaining a fast-growing profit driver.

Just Outside the Top 10: Three More Giants to Watch

While they are no longer in the top 10, these companies remain highly important for traders:

JPMorgan Chase ($837 B)

JPMorgan remains the largest US bank by assets and a key bellwether for the financial sector. It benefits from resilient lending, strong capital markets activity, and a higher-for-longer interest rate environment.

Eli Lilly ($830 B)

Eli Lilly continues to benefit from strong demand for its diabetes and obesity treatments, including Mounjaro and Zepbound. Supply constraints remain a factor, but long-term growth expectations are still strong.

Visa ($611 B)

Visa maintains its dominance as the world’s leading payment network, benefiting from a global shift toward digital transactions and robust consumer spending across its vast merchant ecosystem.

Key Trends from the Top 13

1. Technology Dominance

Technology continues to dominate the upper end of the US equity market.

- 7 of the top 13 companies are technology firms

- AI and cloud computing remain the biggest valuation drivers

- Companies with clear exposure to AI infrastructure or monetisation continue to attract the strongest investor interest

2. AI Is the Biggest Value Driver

The companies benefiting most directly from AI momentum include:

- NVIDIA – core provider of AI training and inference hardware

- Microsoft – monetising AI through Azure and Copilot

- Alphabet – embedding Gemini across Search, Cloud, and Workspace

- Amazon – scaling AI through AWS and custom silicon

- Meta – using AI to improve ad targeting, engagement, and efficiency

3. Sector Distribution

| Sector | Companies |

|---|---|

| Technology | 7 |

| Consumer/Retail | 2 |

| Finance | 2 |

| Healthcare | 1 |

| Energy | 1 |

Final Thoughts for Traders

The top 10 largest US companies by market capitalisation is not just a ranking. It is a snapshot of where capital is flowing and which themes are leading the market.

At the moment, the dominant theme is clear: AI infrastructure, cloud computing, and digital platform strength continue to command premium valuations. For traders, these companies are essential to watch not only for individual stock opportunities, but also for broader signals around sector rotation, volatility, and index direction.

Understanding who leads this list, and why, can offer valuable insight into the forces shaping the market right now.

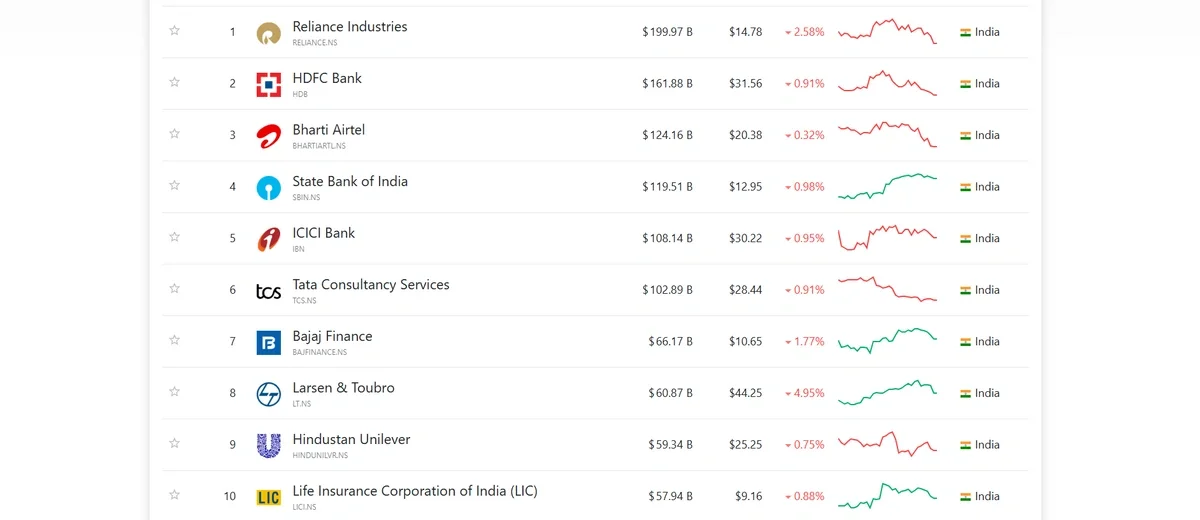

Learn more about the biggest companies in different countries and regions around the world by reading our other articles:

- Top-10 largest non-US companies by market capitalisation

- 10 Biggest UK-based Companies

- Africa’s Top-10: Leading Companies by Market Capitalisation

- Top 10 Largest Latin American Companies

- Top 10 Largest Companies in China

- Economic Powerhouses: Trillion-Dollar Companies Club

- Titans of the East: The 10 Largest Companies Shaping Asia’s Future in 2025

- Top 10 Largest Companies in India

Also, we recommend that you find out with our Who Tops the Global GDP Rankings.

Feeling ready to trade yet? The share prices of publicly traded companies are constantly on the move, providing ample opportunity for traders to take advantage of market movements. Trade these movements today on the MT4 platform. It’s effortless, beginner-friendly, and used by traders across the world.Trade on MT4 with your Hantec Markets trading account today.

Disclaimer: The content of this article is intended for informational purposes only and should not be considered professional advice.