Trading Guides

Exploring the Differences Between MetaTrader 4 and MetaTrader 5: A Comprehensive Comparison

In this article, we will look at the differences between two trading platforms: MetaTrader 4 (MT4) and MetaTrader 5 (MT5).

In this article, we will look at the differences between two trading platforms: MetaTrader 4 (MT4) and MetaTrader 5 (MT5).

OPEC is a powerful oil coalition influencing global prices & supply. Learn how its production decisions impact oil futures, energy stocks, commodities & create trading opportunities.

Understand gearing ratio, a critical metric for traders evaluating leverage and risk. Learn how to calculate gearing, interpret healthy vs. risky levels, and use it to make informed trading decisions. Get insights on optimal gearing for different strategies and assets.

Discover the thrilling world of Boom & Crash indices trading. Master volatile markets with proven strategies for capitalizing on rapid price spikes and crashes.

Use this 20-point checklist to evaluate whether the broker you choose to trade with is safe… or a scam.

2024 Commodity Outlook: Expectations for Oil, Gas, Metals, and Agriculture. Get insider analysis on key factors impacting commodity prices like the Ukraine war, El Niño, Chinese economy, and more. Explore forecasts for gold, copper, natural gas, agricultural commodities, and other major trading instruments.

In this article, we’ll explore the exciting world of bullish and bearish markets. Whether you’re a seasoned trader or just starting, understanding these market dynamics is crucial for success. So, buckle up and let’s dive in!

This article provides an overview of exit strategies in trading and why they are essential for long-term success.

Here’s a look at the top 4 currency pairs that were most commonly traded in 2023: XAUUSD, EURUSD, USDJPY and GBPUSD.

In this article, we unravel the world of swaps in trading: factors influencing the size of a swap to navigating the realm of positive and negative swaps.

In this article, we look at the Elliott Wave theory and how it can help analyse markets to anticipate price fluctuations by observing and recognising recurrent wave patterns.

Whether you are a novice or an experienced trader, the knowledge within these books is a valuable resource for navigating the complexities of the financial markets.

This article will look into the top strongest currencies and how they fit into the ever-changing global financial landscape.

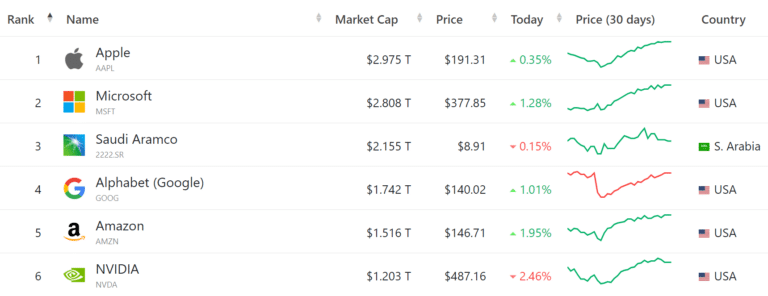

In this post, we explore the largest companies in the world that currently boast a market capitalization of over $1 trillion.

By understanding common scam tactics and following the tips outlined in this article, you can protect yourself from falling victim to fraudulent schemes and become a more informed trader.